For a country where football is one of the last remaining success stories, the resulting blow to morale, and especially the opponents, could not have been more ill-timed.

Unusually rough, perhaps….but the news from Spain has been so consistently bad for so long, that it takes a real whopper of a story to get through the dulled senses of analysts and the populace. I am quite sure that the two football defeats hurt and surprised far more than the earlier news. No one in Europe expected the government to meet its deficit targets. And despite the repetitive and banal pronunciamientos from the Rajoy government about “growth just around the corner” – a broken record inherited from the Zapatero administration – no one expected Spain’s economy to manage even the modest estimate of the Economy Ministry.

For the casual American reader, the depth of Spain’s troubles may come as something of a shock. After all, the Spanish 10-year bond spread with the German Bund has narrowed considerably and wasn’t that the harbinger of doom? Thanks to Super Mario and the OMT, the threat of a debt death spiral has now receded from Europe’s periphery. And Spain has managed to stay out of the headlines recently, thanks largely to Cyprus and Italy’s electoral circus. Pointedly, the Spanish 10-year bond has outperformed its Italian counterpart since the February elections in the latter country threw markets into turmoil.

The bad news from Spain is mostly old news, and so many assume that the country will be able to continue to muddle along. Unfortunately, that assumption may be misplaced. The crisis has not only exposed the papered over structural deficiencies in the Spanish economy; it has thrown a spotlight on the corrupt and dysfunctional public sector, delegitimizing the political institutions that prop up the state. Mr. Rajoy is not noted for a bold, decisive style and he has less room to maneuver than his predecessor did. But his current strategy is condemning his country to at least a decade of stagnation at a time that it cannot afford it.

The really bad news was delivered on Thursday, April 25th. The National Statistics Institute (INE) published the employment situation for the first quarter of 2013[1]. The report is bloodcurdling; but worse than the statistics was the appalling nonchalance of Alfonso Alonso, the Press Secretary for the ruling Partido Popular, whose upbeat reaction to the employment report must have shocked even the most cynical spin doctor. Noting “the improvement in the trend,” [2] Mr. Alonso repeated the hackneyed official line that things were going to improve in 2014 (…2013….2012…2011…2010…). He was promptly castigated by the opposition, though the record of the PSOE in government is at least as dismal.

Apocalypse: Unemployment

Spain’s unemployment rate has reached a historic high of 27.16%, Great Depression levels; 6.2 million people without work. Almost half of the unemployed have been out of work for more than one year and are at risk of becoming “socially marginalized” and of falling out of the economy completely. There are 1.9 million families whose every member is out of work, almost 1 family in 10. For those under 25 years of age, the unemployment rate has increased 4.2% in the last quarter to 57.3%. Yes, read that figure again.

Spanish unemployment is not distributed evenly throughout the country. While 27% sounds, and is, horrendous, regions of southern Spain are suffering nothing short of a cataclysm, with unemployment above 35% in Andalucía, Extremadura, the Canary Islands and the enclaves of Ceuta and Melilla. Such a scale of ruin and suffering is scarcely imaginable.

Spanish unemployment is not distributed evenly throughout the population either. Despite the government’s recent labor market reform, there still exists a two tiered system of contracts. Older workers receive far more in terms of benefits, pay and security; while the young are forced onto temporary contracts that can be terminated with a minimum of hassle for the employer, and often are precisely to prevent these employees from acquiring sufficient seniority to automatically be reclassified as long-term employees. This system is zealously defended by unions and workers groups, who remain a powerful force in Spanish politics. It goes without saying that illegal immigrants are the most exploited of all. The result is the enormous disparity in the unemployment rate by age group:

The employment situation is nothing short of apocalyptic, but not for the reasons that most people might assume. One of the key lessons of the Great Recession is that the welfare state has done its job very well indeed. Can anyone imagine what Spanish levels of unemployment would result in without the benefits of the social safety net provided by the state? We don’t have to imagine it: the last time around, there was civil war and fascism, and not just in Spain. Today, there are protests, some of them large, but no detectable trend towards radicalism and revolution. There is no equivalent to New Dawn or even the Five Star Movement in Spain.

The real danger to Spain is not radicalism or even Catalan independence, an unlikely prospect which may nevertheless come about through the blundering of Mssrs Rajoy and Mas; Spain risks losing time and people. Time to rebuild state finances in general and the social security fund in particular in preparation for the severe greying of the population over the next 20 years. People, because it is the youth and immigrant segments that will enable Spain to pay for all the benefits it has promised its future pensioners, and it is precisely these groups who are emigrating in droves. Who wouldn’t when they have a less than 1 in 2 chance of finding a job?

The Immigration Miracle

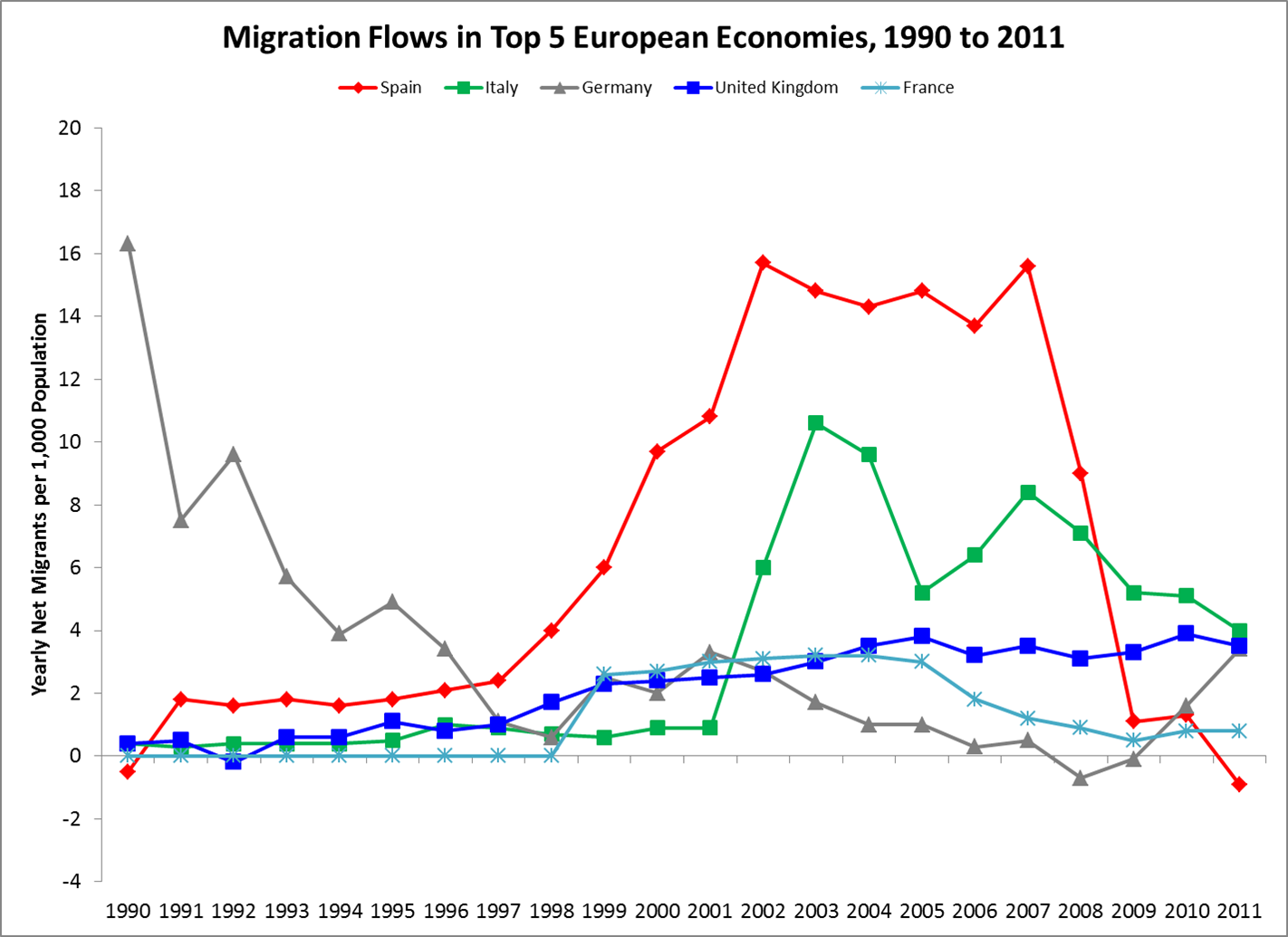

The “Spanish Miracle” of the 2000’s was a miracle of demographics. The fantastic growth of the Spanish economy was due as much to the arrival of over 6 million immigrants as to the arrival of the Euro. In fact, the boom in Spain predates the introduction of the Euro by 5 or 6 years, beginning around 1996. Between 1998 and 2007, the Spanish economy[3] grew on average an enviable 3.8% in real terms (over 5% in nominal terms) and reduced unemployment by over 10%, from 18.7% to 8.3%, while absorbing those 6 million immigrants, almost 15% of the native population. An unparalleled accomplishment for any nation not in the Western Hemisphere[4].

We see some similarities in other European countries[5], though none as pronounced as Spain. Germany enjoyed a growth spurt between 1998 and 2000 which coincided with an uptick in the immigration rates to the country; the United Kingdom has long benefited from a steady influx of immigrants to maintain a level of growth second only to Spain’s amongst the top economies in Europe. Only Italy seems to have missed out in benefiting from their immigration wave between 2002 and 2007: the Italian economy grew on average a meager 1.2% per annum versus 2.1% in the preceding five years.

Immigration, far from being a burden to national economies, is wholly beneficial, especially to those European gerontocracies that have a serious deficit in young workers and collapsing fertility rates. Immigrants act as a “force multiplier” in economies: they don’t get the ball rolling, but once growth starts, they add substantially to it. The more open the economy and society, the more benefit is added. That might help explain the difference in performance between markets: Spain and the UK are (anecdotally at least) more open and receptive to immigrants than Italy or Germany, and so they derive more benefit from their presence through improved integration of these workers[6].

Migration is not a leading economic factor and it is, by definition, highly mobile. Since 2008, the decline in migration to Spain[7] has been even more dramatic than its previous increase. In fact, Spain has suffered the largest reversal in migration flows of any large European economy and of all European economies but two, Ireland and Iceland. Italy and France have also suffered a reduction in immigrant inflows, but remain net recipients for now. Germany is the main winner amongst the large economies; the dramatic increase in migrants to Luxembourg and Cyprus is mostly a factor of those countries’ tiny populations – the total numbers are very small, and we can be confident that if my data series extended into 2013, Cyprus would no longer be first on the list.

Of course, all of this is disastrous news for Spain. While some people may hold the opinion that during the crisis it is better for the foreigners to go home, the fact is that the departure of working age immigrants is reducing the overall potential for growth in the Spanish economy. And it is not just foreign born workers who are departing; increasingly, it is the Spanish themselves who are leaving to look for better opportunities. These youths are indisputably the future of Spain, and their departure leaves Spain permanently the worse off.

The Vanishing Immigrant

So what? Most governments are not keen on having their youth flee the country in droves, especially when these are the best and brightest of their citizens. But won’t they come back when the situation improves? Isn’t this a short-term phenomenon, to be borne with until growth returns to the South, like the swallows of Capistrano? Yes and no.

A scatterplot of net migration versus unemployment from 1990 to 2011 in the Big 5 European[8] economies plus Portugal and the Netherlands gives us some idea of a key relationship between the two variables. They are negatively correlated[9], but the predictive power of unemployment by itself is weak[10] – there is more to the story than just the employment situation in the destination country. Complicating things, the elasticity of migration is not constant between the different markets. There is a group of 4 “elastic markets” (Germany, Spain, Italy, Portugal) where migration is quite responsive to the local unemployment rate, and 3 “inelastic markets” (UK, France, Netherlands) where migration remains relatively constant despite changes in the unemployment rate.

Spain belongs to the “elastic markets” and a logarithmic trend line seems to fit the observed data points better than a linear one. We are “lucky” in that Spain has passed through two crises and one significant growth phase during the observation period, so we can test if net migration today is conforming to its previous behavior during the high unemployment years of the early and mid-1990’s.

Preliminary reports of net migration for 2012 are not encouraging. The National Institute of Statistics (INE) reported a net decrease in the number of registered foreign residents in Spain of -216,125, along with an increase in the number of Spaniards living abroad of +114,413 for a total net migration of -330,538. That’s equivalent to a net migration rate of -6.99 per 1,000 inhabitants and much higher than the model’s predicted value of -2.94 per thousand[11]. This is undoubtedly due to the fact that the youth and immigrant unemployment rates are both so much higher than the average unemployment rate across all sectors. In fact, the model’s estimate (-139,000) is almost identical to the Short-term Population Projections 2011 to 2021 of the INE (-122,000)[12], though the INE uses a more complex methodology[13].

The implications of this are serious. Assuming that unemployment remains above 20% throughout the rest of the decade – and there is every reason to believe that it will[14] – it means that Spain can expect to lose between 1 and 1.8 million people before 2020[15].

To make matters worse, the combination of Spain’s low fertility rate, aging population and the emigration of higher fertility foreign women are estimated to cause deaths to exceed births for the first time in 2019 and accelerating thereafter. Given that mortality and fecundity rates are both well-studied and highly resistant to change, the only way to turn this trend around is to have more women immigrate to Spain. An unlikely prospect through the end of this decade.

Emigration of the working age population, especially the young; a long-term fall in the arrival of new immigrants; a continued fall in the birth rate: the result is that Spain’s population will continue to grow older on average, putting enormous pressure on the country’s finances. How will the government pay for all of the people who are retiring or out of work? How will it fund education and productivity enhancing R&D? The simple answer is that, increasingly, it will not be able to.

Fraying, Fraying, Gone: the Social Safety Net

Whatever the burden today on the long-suffering Spanish middle and lower classes – in other words, the primary contributors to government tax revenues – there is no relief in sight. Like Mr. Montoro’s elusive promise to reduce tax rates: after the 2013 deficit targets have been met; in 2014; when the crisis is over… the Spanish worker will likely be rewarded by empty promises. Full disclaimer: I am an interested party, being a middle class taxpayer in Spain, much to my lamentation. The reason for this has less to do with the inveterate wickedness of the politicians than with the simple logic of the dependency ratio.

The dependency ratio compares the size of the dependent population (those under 16 and those over 65 years old) with the working age population (everyone in between)[16]. It is a useful measure of the “burden” on the work force to maintain the “unproductive” segments, though not without its detractors[17]. The smaller the ratio, the better: that implies that there are lots of workers supporting relatively few dependents. Since not all dependents are the same, and the costs of the benefits they receive is different, it is usual to talk about an “old age” dependency ratio and a “child” dependency ratio, with the implication that the former is more burdensome than the latter.

Imagine three economies composed of 100 people each.

Economy A has 75 workers and 25 dependents; the dependency ratio = 33

Economy B has 50 workers and 50 dependents; the dependency ratio = 100

Economy C has 25 workers and 75 dependents; the dependency ratio = 300

It is obvious that the workers of Economy A need to dedicate fewer resources per worker (i.e. pay fewer taxes) to support their dependents. It is also clear that the workers of Economies B & C need to pay more, both per capita and in total. That is not necessarily a problem: Economies B & C could be very wealthy ones, with high wage rates; or else worker productivity may be very high compared to Economy A. That is in fact what you see in the world today: if you think of Economy A as “India”, Economy “B” as the United States, and Economy C as “Japan”[18], it becomes clear why the value of the dependency ratio has little meaning by itself.

Still, economists agree that a high dependency ratio is generally a bad thing since it not only increases fiscal outlays in social benefits and spreads that tax burden over a smaller number of workers, it also generally leads to reduced levels of consumption and an overall slowdown in economic growth. There is a significant literature on the subject: Dr. Paul Krugman has written of the “shortage of Japanese”[19] to describe the main source of that nation’s ills; Robert Gordon has spoken of the “end of growth”[20], while Edward Hugh has written extensively on the demographics of Portugal[21], Japan and Spain[22].

According to the World Bank[23], whose dependency ratio calculations should be taken with caution, Spain has the 17th highest dependency ratio in the world in 2011. It is significant that, with the exception of Japan at #1, every other nation in the top 20 is in Europe. In fact, in the top 40 nations, there are only 6 that aren’t in Europe: Japan (1), Uruguay (26), Canada (30), Australia (33), New Zealand (35) and the United States (37). It gives a new meaning to the phrase the “Old Continent” and calls into question the sustainability of Europe’s social welfare model.

Spain’s example remains particularly relevant. The evolution of the dependency ratio markedly shows the effect of immigration: the wave of immigrants to Spain in the late 1990’s and early 2000’s reversed the thirty year trend towards increased dependence; only the interruption wrought by the Spanish housing bubble and Euro crisis has caused this mechanism to reverse itself.

Returning to our migration model prediction, in the worst case, Spain stands to lose about 1.8 million inhabitants by 2020, mostly immigrants who relocate. That causes Spain’s population to fall from 46.2 million in 2012 to an estimated 44.3 million in 2020. The emigrants are mostly of working age, which adversely affects the dependency ratio:

The total dependency ratio increases from 48 to 54: notice that it is even higher when we exclude the immigrant population, because of the lower fertility of the indigenous population. Notice also that the whole increase is coming from the aged dependency ratio: this is not more children being born, it is more people retiring.

I also calculated an “adjusted” dependency ratio, which takes into account the average unemployment rate per quinquennial age group to calculate the actual burden imposed on employed workers. The ratio surges to 119, which can also be read as meaning that each employed worker is supporting 1.2 underage, unemployed or retired dependents. By 2020, the adjusted ratio falls to 108, assuming the unemployment rate falls as predicted by the IMF. It should be evident from a simple calculation of average yearly benefits paid out compared to the average yearly income of a Spanish worker that this level of support is unsustainable.

What can the government do? If the social safety net implicit in the welfare state is what has kept the lid on social unrest in Southern Europe, and if that net is fraying in the most affected countries like Greece, Spain and Portugal, what steps should governments take?

The obvious step of raising taxes has already been applied. That helps fund the current benefits at the cost of consumption, corporate profits and growth. Further tax increases are unlikely, and even if applied, they will cost the economy more than the revenue they will raise for government. Cuts to benefits are the only alternative, and those are also being enacted:

- Unemployment benefits are set to automatically expire and, despite some extensions by the past and present governments, the percentage of unemployed workers receiving benefits has plummeted to 63.3% from 80.9% in 2010[24]. That’s about 2.2 million people left to their own devices, but who aren’t draining the state’s coffers;

- The government can, and already has, extended the retirement age. From 65 it has moved to 67; we can confidently expect it to continue to climb as both medical technology advances and fiscal resources retreat apace. Moving the retirement age from 65 to 70 would impact another 2.2 million people in 2012, up to 2.35 million in 2020. A further advancement from 70 to 75 seems highly unlikely and too politically charged to be practicable in the near future, but it would impact a further 1.74 million in 2012 and up to 2.1 million in 2020.

The overall impact on the adjusted dependency ratio would be to bring it down from 119 to 98, which is still high; but desperate times call for desperate measures. And this crisis might just be viewed as the perfect political cover to institute needed pensions reforms to make these sustainable in the long-run. After all, the demographic crisis is not going away even if the economic crisis does.

The Lost Decades

Spain faces the almost certain prospect of economic stagnation, high unemployment and declining standards of living for the foreseeable future. This is the price of participating in a currency union with a productivity juggernaut like Germany. The extremely high rates of GDP growth of the late 1990’s and 2000’s were fueled by Spain playing “catch up” to the European mean through convergence funds, the risk premium from joining the Euro, and the access to German savings on “easy term” that led to the inflating of the property bubble. None of these phenomenon can be counted on to deliver high rates of growth in the future. What’s left? Innovation and worker productivity enhancements? In neither field can the periphery compete with the center.

Spain is not going to become a high-tech innovation or manufacturing center when Germany is putting out 15x more patents and 7x more high technology patents per year. Mr. Rajoy’s government has already announced further cuts to the government’s R&D budget in an attempt to meet the austerity targets imposed by Brussels and Berlin. These austerity measures, which were supposed to restore business confidence, wage competitiveness and hence growth, have so far failed to deliver on any of the three measures:

Despite important gains amongst Spanish workers in terms of output and labor costs, Germans are still far more productive per hour worked; the Spanish labor cost index must fall far further before Spain could be considered competitive against Germany. Assuming the Germans don’t continue to invest in productivity and competitiveness in the meanwhile. These results have been purchased with enormous pain to Spanish workers and their families. Can European governments really believe that this is sustainable over another decade?

Political systems are vulnerable to “tipping points”, just like economies or stock markets: moments when an unseen frontier is crossed, causing a self-reinforcing trend to begin and accelerate. Just like bears seizing control of a faltering market, the change can come swiftly and bring devastating results. This explosive combination exists in Europe’s periphery, awaiting the unknown catalyst that will set it off. Since Europe is a political experiment, the detonator must also be political, not economic: the social mayhem of profound, enervating unemployment and the inevitable necessity to cut social welfare benefits are the two best candidates. We hold our breath during each new election in the periphery: Spanish regional and general elections are not due until 2015.

Sources and Notes:

[1] “El paro supera los 6,2 millones y alcanza el 27,16% de la población,” Intereconomía, 25 April 2013 (Spanish only)

[2] “Reacción de PP, oposición y sindicatos a los datos del paro,” Europapress, 25 April 2013 (Spanish only)

[3] Eurostat data. Extracted on 14 May 2013.

[4] The United States, Argentina, Uruguay, Chile, Brazil and some of the Caribbean Islands have had comparable levels of growth and immigration in the late XIXth and early XXth centuries.

[5] The French data series for net crude migration is missing from 1990 to 1998, making comparison difficult.

[6] Language and shared history undoubtedly play a role: Spanish migrants are mostly from Latin America, and share a language, religious and historical ties. Similarly, most UK migrants are, or used to be, from former Commonwealth nations. Germany and Italy have almost no former colonies to draw migrants from: their migrations come from Turkey and Eastern Europe, where the language, customs and even religions are dissimilar.

[7] See note 3.

[8] Eurostat data is used for Germany, Italy, Portugal, Spain, Netherlands and UK. The French data series was not available before 1999 on Eurostat, so I used the U.S. Census Bureau International Programs database which is based on French data from the Institut National de la Statistique et des Etudes Economiques (INSEE).

[9] The correlation coefficient is -0.305, meaning as unemployment increases, migration decreases, but by a lesser amount. The correlation coefficient can take any value between +1 and -1.

[10] The differences in market characteristics and the complexity of migration behavior preclude a unified model for all of the markets studied. However, the significance of unemployment in each individual market seems substantial, Spain for example:

It is not my intention to build a migration regression model in any case, only to estimate whether net migration is likely to become positive again, and when, based on the employment situation in Spain.

[11] Using the average unemployment value of 25.2% for 2012 (Eurostat).

[12]1.7. Inmigraciones procedentes del extranjero, por sexo, edad y año; 1.9. Emigraciones con destino al extranjero, por sexo, edad y año, Proyecciones de población a corto plazo. 2011-2021, Instituto Nacional de Estadística.

[13] For a full discussion of the methodology used by the INE for the Short-Term Population Projections, see their Methodological Briefing (Spanish only).

[14] The IMF estimates Spanish unemployment to remain well above 20% through 2018, the last year of the forecast. It should be noted that the IMF has been consistently underestimating the GDP and unemployment effects of European austerity since 2008. World Economic Outlook Database, April 2013. Extracted on 21 May 2013.

[15] There is a discrepancy between the different data sources within the INE. The Estimation of Current Population provides a total of 46.196 million inhabitants, in line with the IMF and U.S. Census Bureau’s data. However, the Municipal Registrar Statistics (Estadística del Padrón Continuo) provides a higher figure of 47.265 million. I have used the lower of the two.

[16]

[17] Critics of the dependency ratio argue that the cut-offs are too arbitrary: after all, many people over the age of 65 continue to work and be “productive”, more every day. It also does not take into account that not everyone in the “productive” age groups is actually producing: the unemployed, specifically, are not contributing to support the system, but are dependent on it. Like GDP, it is still a useful convention.

[18] There are no cases in the real world as extreme as those in the example. That country with the highest dependency ratio today is Japan and the actual dependency ratios for 2011 are: India ( 8), United States (20), and Japan (37). World Development Indicators, The World Bank. Extracted on 21 May 2013.

[19] Krugman, Paul, “The Japan Story,” The New York Times, 5 February 2013

[20] Gordon, Robert, “The death of innovation and the end of growth,” TED Talks, April 2013

[21] Hugh, Edward, “Does Portugal Have Its Own ‘Shortage of Japanese’ Problem?” Economonitor, 12 May 2013

[22] Hugh, Edward, “Does Emigration Put Spain’s Health and Pension System At Risk?” Economonitor, 26 March 2013

[23] See note #18 for source. A comparison of the World Bank’s dependency ratio for Spain with the actual population statistics supplied by the Spanish National Statistics Institute shows a large discrepancy in the two calculations. The World Bank’s 2011 estimate of 25.3 is slightly more than half the value calculated by INE of 49.4 for the same year.

[24] Jiménez, Miguel, “El número de parados registrados sin prestación bate un nuevo record,” El País, 2 April 2013 (Spanish only)

Thanks Fernando, for another excellent article. Crystal-clear and well documented, as usual.

Posted by Cedric Thiery | May 24, 2013, 04:28